Sources: Central Statistics Agency (BPS)

Inflation (YoY): In June 2026, Indonesia’s inflation rate is 3.34% year on year, down from the peak earlier in the year but still higher than levels recorded throughout most of 2024 and 2025. The initial increase was mostly driven by a low base impact following the -0.09% deflation in February 2025, whereas the recent moderation implies that transient statistical effects are diminishing. Inflation has settled to a more moderate level compared to the five-year trend, but it remains above the extraordinarily low inflation environment of 2024-2025, indicating that underlying price pressures should be closely monitored.

Source: Bank Indonesia

Currency Rate (USD/IDR): The rupiah drops to its lowest point in the five-year period displayed in June 2026, at about IDR 17,899 per US dollar. In contrast to the rather stable IDR 14,000–15,000 range in 2021–2023 and the progressive depreciation observed through 2024–2025, the most recent significant decrease suggests that external pressures, such as a stronger US currency, higher global interest rates, or capital outflows, are becoming more intense. A declining value of the rupiah increases the cost of imports and the servicing of external debt, raising the possibility of imported inflation and creating problems for macroeconomic stability.

Source: Bank Indonesia

BI Rate: In June 2026, Indonesia‘s BI Rate stands at 5.75%, following a sharp increase from 4.75% in May 2026. Compared with the past five years, the latest rate returns to the restrictive levels seen during the 2023–2024 tightening cycle after a period of monetary easing in 2025. The hike reflects the central bank’s stronger focus on stabilizing the rupiah and containing inflationary pressures amid heightened external risks.

The 1-month deposit rate: The 1-month commercial bank deposit rate is 4.20% in March 2026 (the most recent deposit rate displayed), which is lower than the highest levels seen in 2023–2025 and down from almost 4.9% in mid-2025. Deposit rates are still higher than the accommodating levels of 2021-2022 relative to the five-year trend, but they have not yet reacted to the most recent increase in the BI Rate, indicating a delay in banks’ repricing of deposits as they balance funding costs and liquidity constraints.

Source: S&P Global PMI

The Manufacturing PMI for Indonesia is 46.9 in June 2026, which is below the 50-point mark for the third straight month and indicates that manufacturing activity is still declining. The most recent figure indicates a significant deterioration in business conditions when compared to the five-year trend, during which the PMI often remained over 50 and showed consistent expansion aside from brief downturns. The continuous sub-50 level indicates slower production, weaker demand, and cautious business sentiment, underscoring the growing difficulties facing the manufacturing sector in the face of a less encouraging local and international climate.

Source: Central Statistics Agency (BPS)

Indonesia’s non-oil and gas exports reach US$22.4 billion in May 2026, while imports increased to US$20.3 billion, creating a US$2.2 billion trade surplus. In contrast to the five-year trend, imports continue to be high, indicating strong domestic demand and investment activity, while exports continue to be robust despite declining from their 2025 highs. The surplus is still positive even though it has decreased from the higher surpluses seen in 2021–2025. This shows that export revenue growth continues to outpace import growth and sustain Indonesia’s external balance.

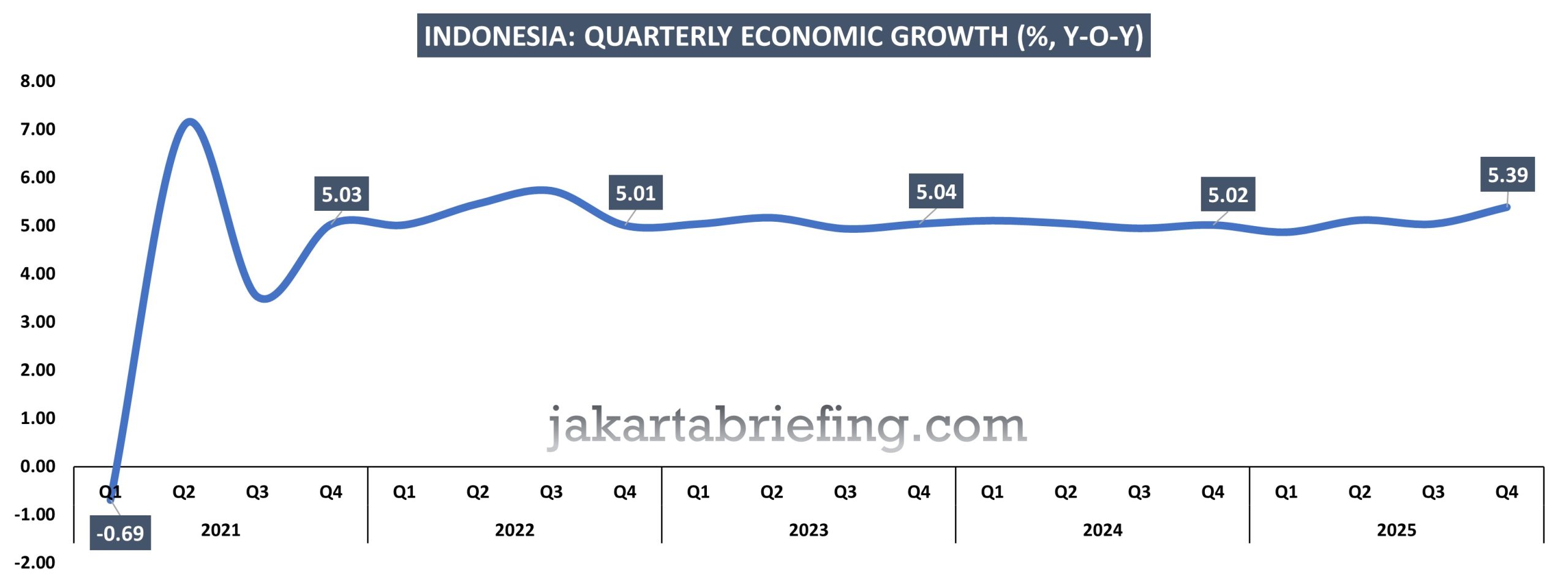

Source: Central Statistics Agency (BPS)

In Q4 2025, economic growth in Indonesia reaches 5.39% YoY, slightly above the ~5.0% range that has characterized the post-pandemic period. Over the past five years, growth rebounded sharply from a contraction in early 2021 to above 7% in Q2 2021, before stabilizing around 5% during 2022–2024. The latest figure indicates a modest strengthening of momentum compared to this stable trend, suggesting resilient domestic demand and a steady recovery path, albeit without returning to the exceptional rebound seen in 2021.

Source: Central Statistics Agency (BPS)

In 2025, economic growth in Indonesia stands at 5.11% YoY, broadly in line with its pre-pandemic average and slightly higher than the relatively stable ~5.0% range observed since 2023. Over the past decade, growth was consistently around 5% during 2016–2019, plunged to -2.07% in 2020 due to the pandemic, and then rebounded to a peak of 5.31% in 2022 before stabilizing again. The latest figure confirms that Indonesia has returned to its steady, trend growth path, indicating resilience and macroeconomic stability, albeit without a significant acceleration beyond its long-term norm.