Sources: Central Statistics Agency (BPS)

Inflation (YoY): Year-on-year inflation reached 3.48% in March 2026, marking a clear rebound from the unusually low -0.09% trough in early 2025 and the ~1–2% range that dominated much of 2024. Compared to the five-year trend, the current level sits in a moderate band—well below the ~6% peak in 2022–early 2023 (driven by post-pandemic and energy price shocks), yet higher than the disinflation phase of 2024–2025. The recent uptick suggests renewed demand-side pressure or normalization of administered prices, but inflation remains broadly within a manageable corridor, indicating a transition from a low-inflation environment back toward a more typical 3–4% range rather than a return to past volatility.

Source: Bank Indonesia

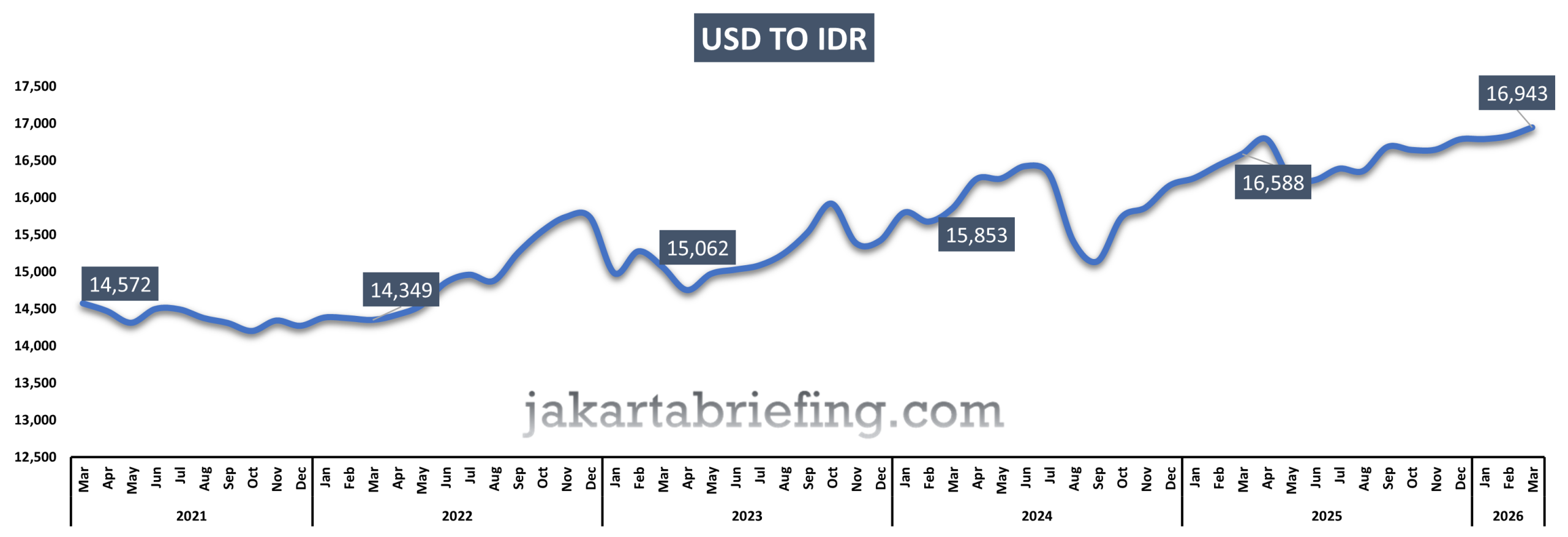

Currency Rate (USD/IDR): By March 2026, the USD/IDR exchange rate reached 16,943, marking the weakest point for the Rupiah in the five-year period and reflecting a clear depreciation trend. While the currency briefly strengthened between March 2021 (14,572) and March 2022 (14,349), it has since steadily lost value, climbing past 15,000 in 2023, 15,853 in 2024, and 16,588 in 2025. The acceleration of depreciation after 2024 highlights mounting external and domestic pressures, with the March 2026 figure underscoring a sustained weakening trajectory compared to the relative stability seen earlier in the period.

Source: Bank Indonesia

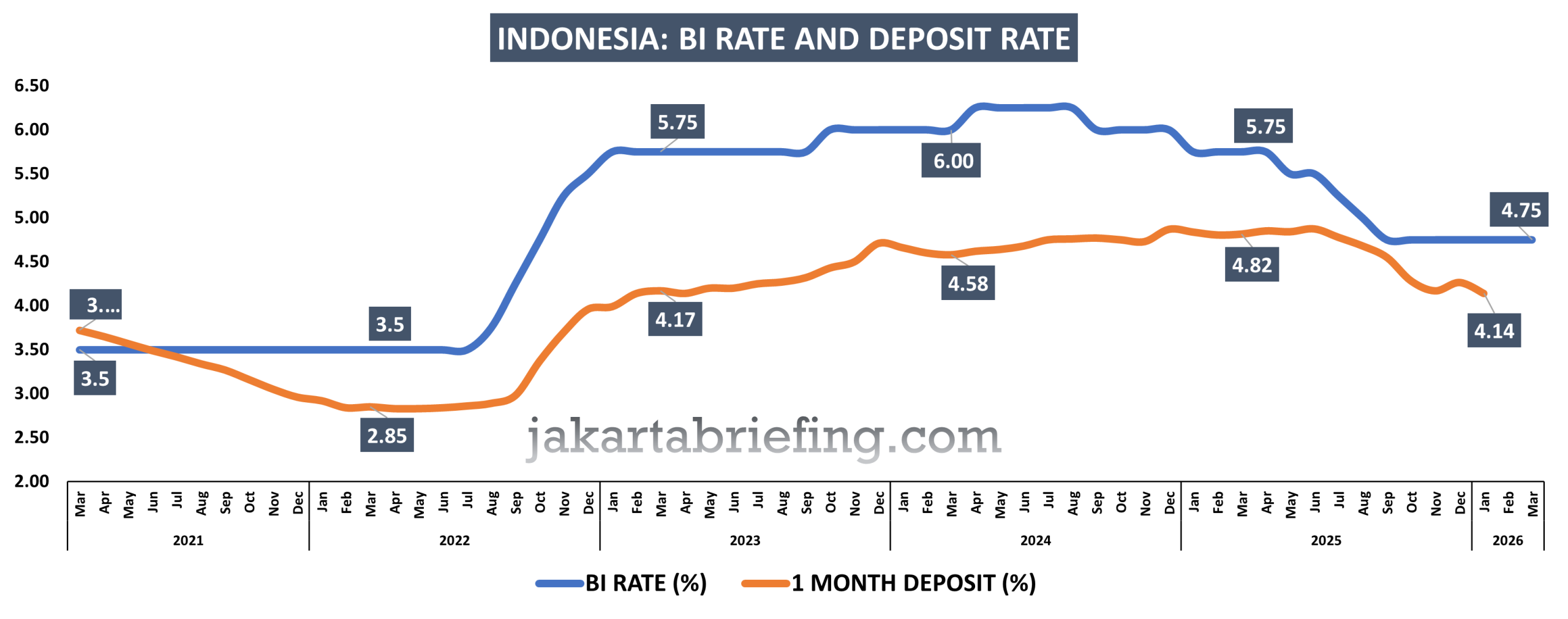

BI Rate: the latest figure in March 2026 stands at 4.75%, which marks a significant decline from its peak of 6.00% in November 2023. Over the five-year span, the BI Rate was stable at 3.5% until mid-2022, then surged sharply to 5.75% by September 2022 and peaked at 6.00% in late 2023, reflecting tightening monetary policy. Since then, it has gradually eased, showing a clear downward trajectory into 2026, signaling a shift toward more accommodative policy.

The 1-month deposit rate, the January 2026 figure is 4.26%, slightly lower than the 4.81% recorded in January 2024 and the 4.60% in late 2023. Over the five years, deposit rates fell sharply from 3.88% in early 2021 to 2.84% in early 2022, then recovered gradually in line with BI Rate hikes, peaking near 4.81% in 2024. The modest decline into 2026 suggests banks are adjusting to the BI Rate’s easing trend, maintaining deposit rates at relatively stable but slightly lower levels compared to the tightening cycle peak.

Source: S&P Global PMI

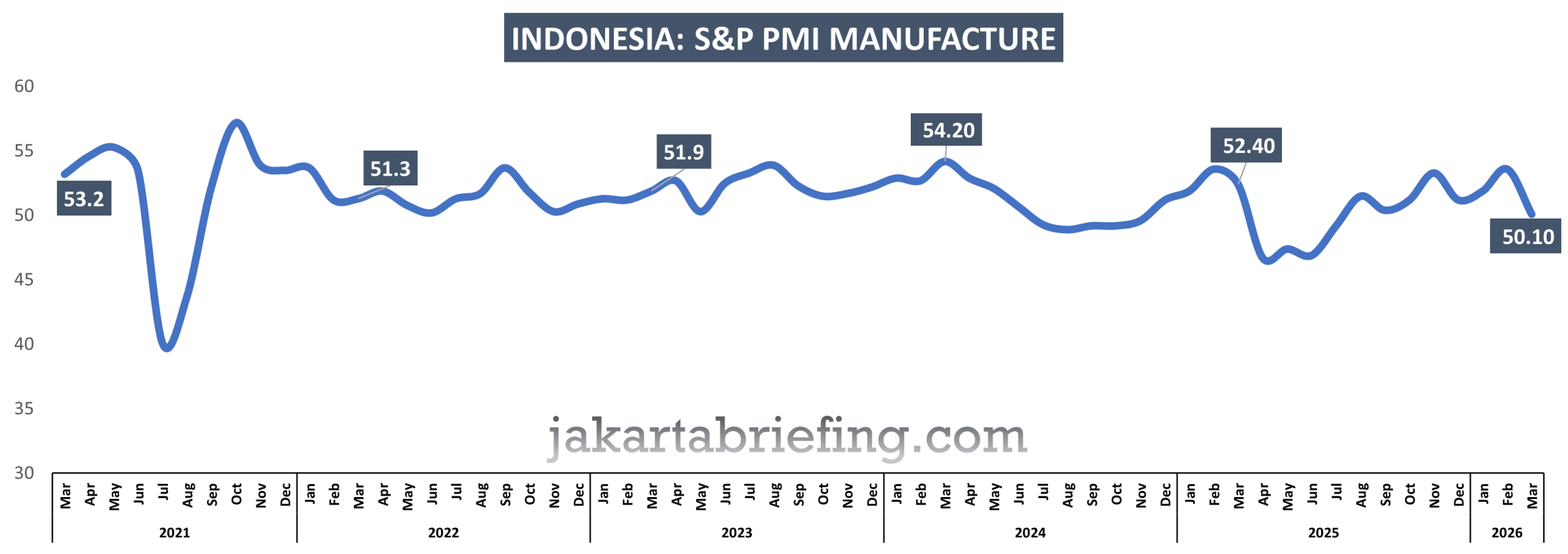

By March 2026, Indonesia’s manufacturing PMI dropped to 50.1, its weakest point in the five-year span and hovering just above the threshold that separates expansion from contraction. This marks a sharp decline from the strong expansionary phase seen in March 2024 (54.2) and contrasts with earlier resilience in 2021 (53.2) and moderate stability in 2022–2023 (around 51–52). The latest figure signals a slowdown in manufacturing momentum, suggesting that after periods of robust growth, the sector is facing renewed pressures that have eroded confidence and activity compared to the upward peaks of the previous years.

Source: Central Statistics Agency (BPS)

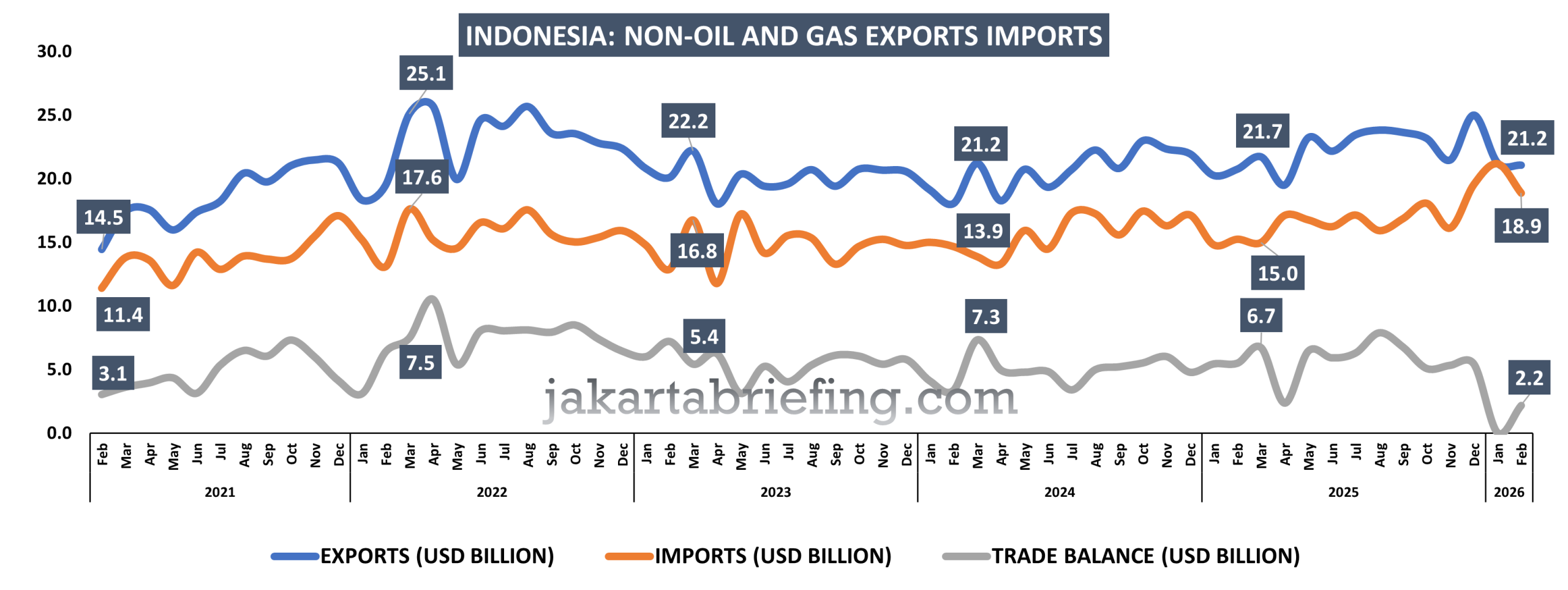

In January 2026, non-oil and gas exports in Indonesia reach about US$21.3 billion, while imports climb almost equally to US$21.2 billion, leaving the trade surplus nearly flat at around US$0.06 billion. Compared with the past five years, exports remain relatively strong and broadly in line with the US$19–23 billion range seen since 2022, but the sharp rise in imports has significantly narrowed the trade surplus. This contrasts with the earlier period of 2021–2024 when Indonesia consistently recorded surpluses of roughly US$3–6 billion, indicating that stronger domestic demand and import growth are now eroding the external buffer despite stable export performance.

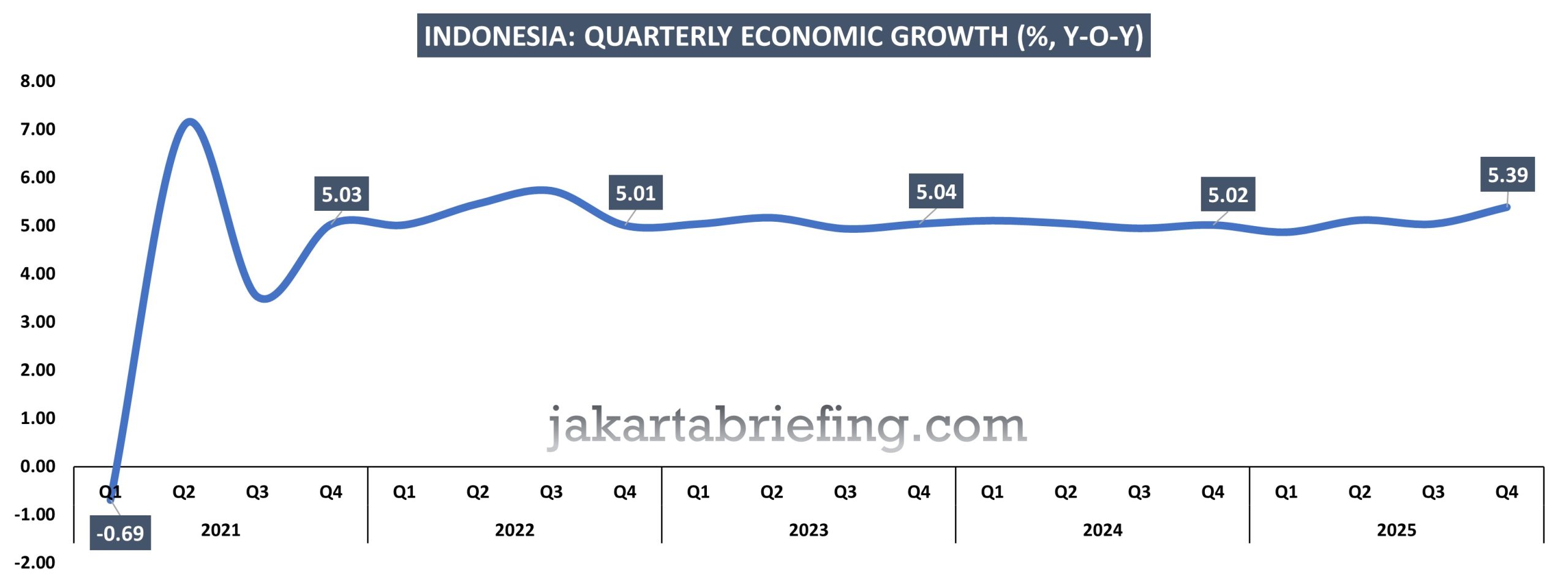

Source: Central Statistics Agency (BPS)

In Q4 2025, economic growth in Indonesia reaches 5.39% YoY, slightly above the ~5.0% range that has characterized the post-pandemic period. Over the past five years, growth rebounded sharply from a contraction in early 2021 to above 7% in Q2 2021, before stabilizing around 5% during 2022–2024. The latest figure indicates a modest strengthening of momentum compared to this stable trend, suggesting resilient domestic demand and a steady recovery path, albeit without returning to the exceptional rebound seen in 2021.

Source: Central Statistics Agency (BPS)

In 2025, economic growth in Indonesia stands at 5.11% YoY, broadly in line with its pre-pandemic average and slightly higher than the relatively stable ~5.0% range observed since 2023. Over the past decade, growth was consistently around 5% during 2016–2019, plunged to -2.07% in 2020 due to the pandemic, and then rebounded to a peak of 5.31% in 2022 before stabilizing again. The latest figure confirms that Indonesia has returned to its steady, trend growth path, indicating resilience and macroeconomic stability, albeit without a significant acceleration beyond its long-term norm.